When recipients ask, “Where’s my money?”, payout speed has already become part of your product.

Recipients want more choice in how they get paid and faster access to their funds—and with our latest release, you can give them both without added complexity.

We’re introducing new payout methods, including debit card payouts (also known as push-to-card payouts), to give your US-based recipients a familiar way to receive funds via a supported Visa or Mastercard debit card—typically within minutes.

At launch (May 7, 2026), this feature is available to US merchants on Cross River Bank (CRB) paying US recipients.

What we cover

Debit card/push-to-card payouts at a glance

- Availability: US merchants (CRB) → US recipients

- Speed: Typically within minutes (card eligibility dependent)

- Supported cards: Visa and Mastercard debit cards

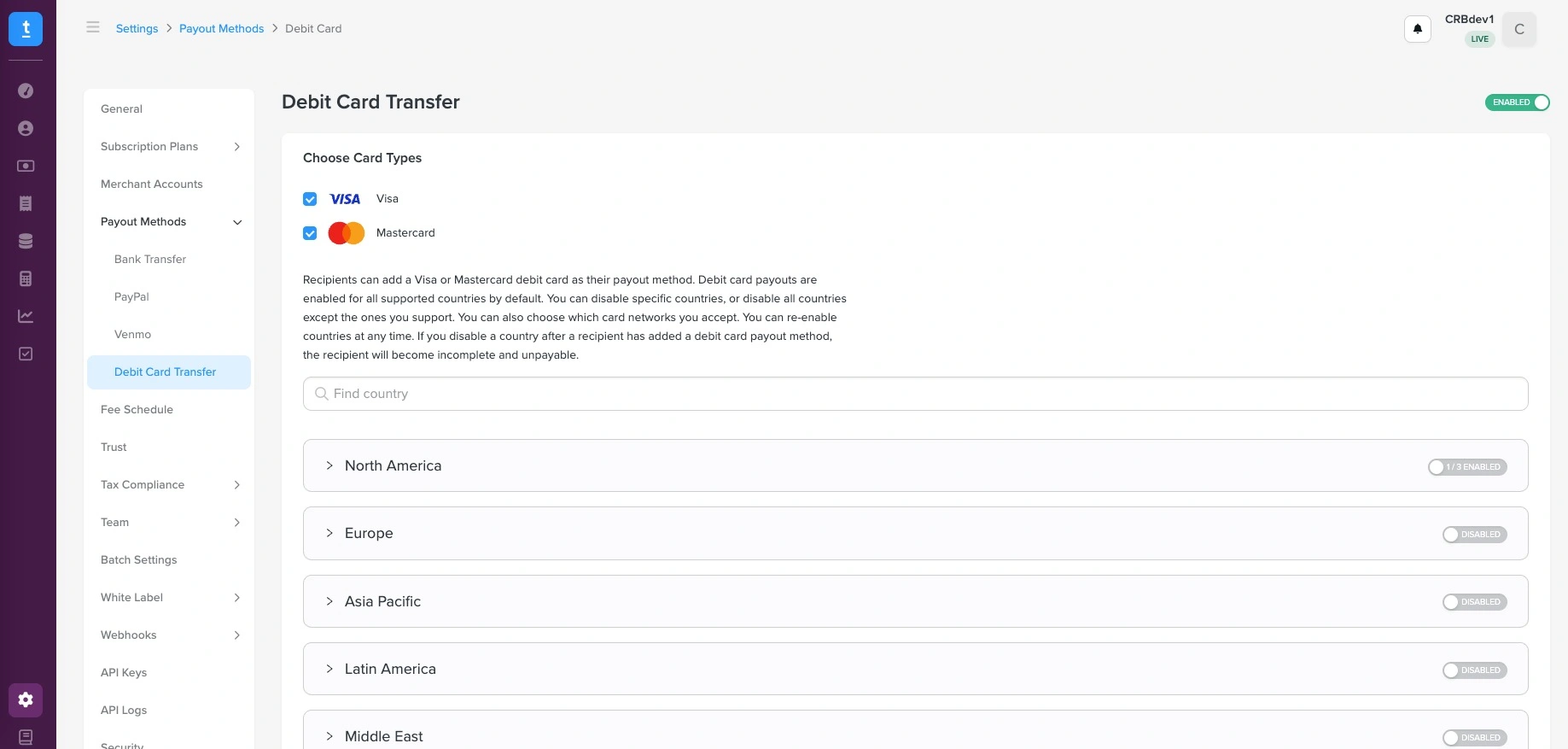

- Networks: Powered by Visa Direct and Mastercard Send

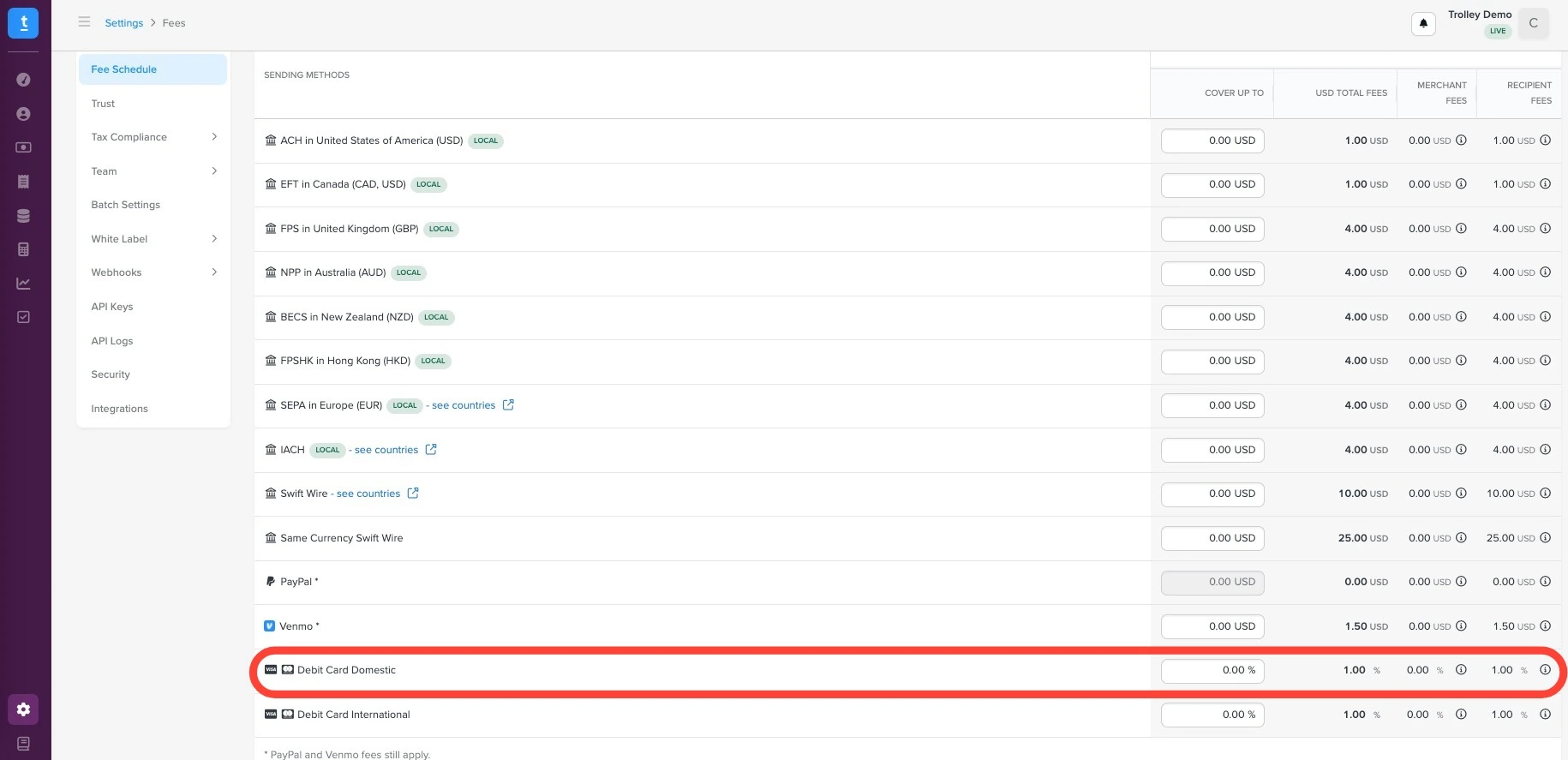

- Fee: 1.00% per payout ($1.50 minimum)

- Funding: From your Trolley balance

- Setup: Dashboard → Payout Methods

- API support: Yes (debit-card method)

What are debit card payouts?

Debit card payouts (often called push-to-card payouts) send funds directly to a recipient’s bank account via their debit card.

That means:

- No bank processing windows

- No waiting for settlement cycles

- Faster access to funds

If a recipient’s card is eligible, they can receive funds within minutes.

Why add debit card payouts?

1. Faster access, fewer delays

Debit card payouts are designed for near-instant delivery. Funds typically available within minutes, depending on compliance screening, the card network, and eligibility. This is a meaningful shift from payout methods that rely on batch processing or bank settlement windows.

For recipients, this means they can access earnings almost immediately after a payout is sent—whether that’s for covering expenses, reinvesting into their work, or simply having greater financial flexibility.

For businesses, faster delivery allows you to close books faster, cuts down on “where’s my money?” inquiries, and reinforces trust by aligning payout speed with recipient expectations.

2. A simpler experience for recipients

How payouts are received matters just as much as when they’re delivered.

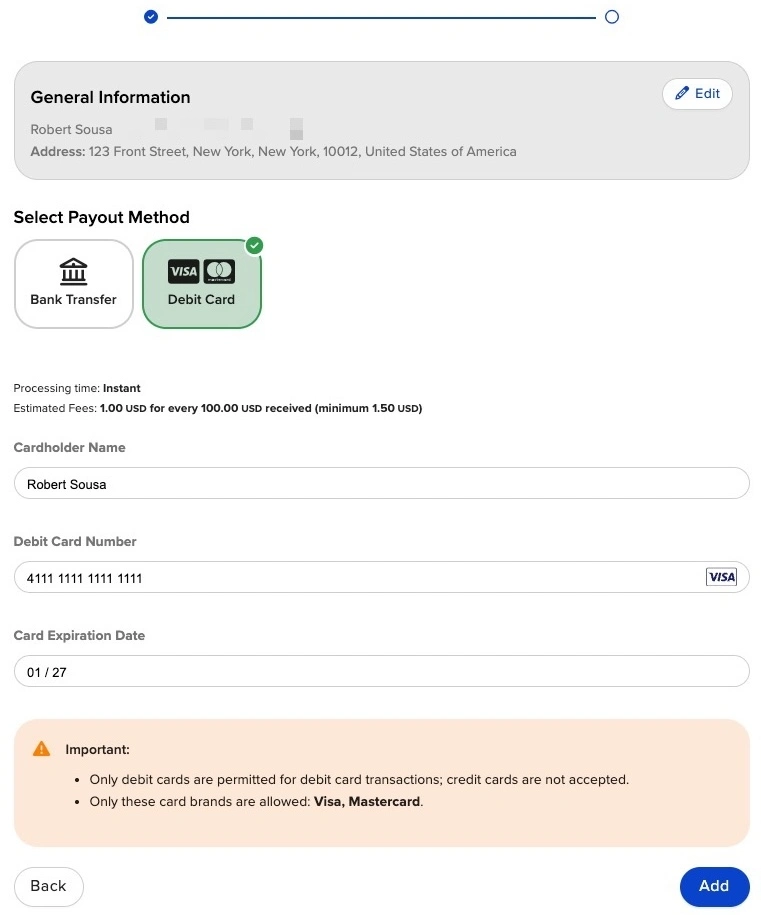

Debit cards are widely adopted, familiar to recipients, and simple to enroll and use. Within the recipient portal, they can add a debit card by entering their cardholder name, card number, and expiry date, with built-in validation to ensure the card is eligible. Unlike bank account details, which are harder to recall and more error-prone, debit card details are typically more accessible and easier for recipients to provide accurately.

Trolley supports physical and digital debit cards eligible for Visa Direct and Mastercard Send payouts.

3. Clear control for finance teams

Speed doesn’t come at the expense of control.

Debit card payouts are fully configurable within your existing payout framework. Finance and AP teams can manage availability within your payout configuration and select supported card networks (Visa and Mastercard).

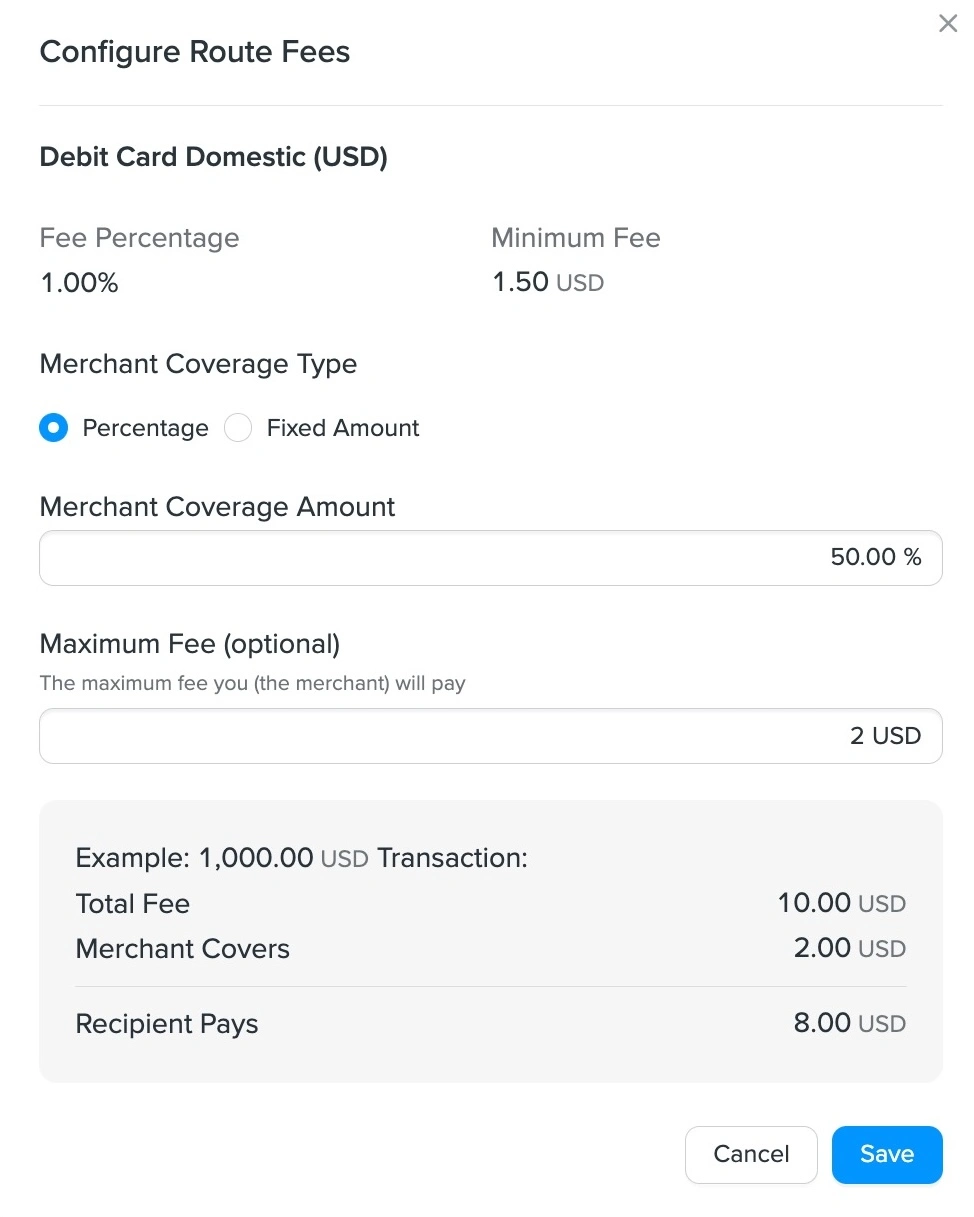

You also maintain control over how fees are handled. Debit card payouts use a percentage-based pricing model (1.00% of the payout amount, with a $1.50 minimum). From there, you can decide how much of that fee to absorb versus pass on to recipients.

Coverage can be configured as:

- A fixed dollar amount per payout

- A percentage of the total fee

You can also apply caps when using percentage-based coverage to keep costs predictable on larger payouts. If you are covering fees on bank transfers, you can choose to cover only that amount and pass the rest on to recipients, allowing you to contain costs while offering a premium, faster payout option.

This flexibility allows you to align payout economics with your business model while maintaining transparency for recipients.

4. Fewer support tickets, faster resolutions

Support teams often bear the brunt of payout friction—especially when recipients are unsure how long a payout will take or whether it was successful.

Common issues like:

- “Where’s my money?”

- “Did my payout go through?”

- “Why did my payout fail?”

are often driven by unclear delivery timelines or payout methods that recipients don’t fully understand.

Trolley’s newest product updates address this in two ways. First, near-instant processing for debit card and wallet payouts reduces the waiting period where uncertainty typically builds. Second, upcoming payment visibility complements this by letting recipients view upcoming payments before they’re processed, while the portal continues to show completed payouts.

Together, this reduces inbound support volume and makes it easier for teams to resolve the issues that do arise.

5. A flexible payout strategy on one platform

There’s no single “best” payout method—only the right method for each recipient and their particular use case.

Debit card payouts give you another lever to optimize your payout strategy alongside existing rails. For time-sensitive payouts, you can prioritize speed with debit cards. For cost-sensitive scenarios, you can continue to rely on lower-cost methods. And for recipients, having the ability to choose increases the likelihood that payouts are completed successfully.

Because this is managed within Trolley, you don’t need to introduce additional providers or workflows. You can offer multiple payout options while keeping configuration, reporting, and reconciliation centralized.

Debit card payouts vs other payout methods

Each payout method Trolley offers solves a different problem.

| Best for: | Delivery: | Cost: | |

| Debit card payouts | speed | minutes | percentage-based |

| Bank transfers (ACH) | cost efficiency | 1–3 days | flat fee |

| PayPal / Venmo | ease for merchants | fast | varies |

| Mobile wallets | familiarity + speed | instant / minutes | percentage-based |

How it fits into your existing workflow

Debit card payouts are designed to fit into your existing Trolley setup without requiring major changes to how you manage payouts.

From a funding perspective, payouts are still drawn from your Trolley balance, and they can be included in the same batch workflows you already use. The key difference is the payout method selected for each recipient.

On the recipient side, the experience is handled within the existing portal. Recipients can add a debit card, complete any required validation steps, and select it as their payout method. If the method is enabled but a recipient has not completed setup, they may appear as incomplete until their details are provided.

From an operational standpoint, payout status tracking remains consistent. You can monitor payouts through the same lifecycle states, while recipients see clear status updates in their view of the portal.

For developers, support is built directly into the API and webhook layer. This includes a new payout method value in all areas where the Recipient Account object is surfaced (debit-card).

These changes are additive and backward compatible, meaning existing integrations will continue to function while supporting the new method. You can find more information on enabling card payouts and handling payout lifecycle events in our API and webhooks developer documentation.

Get started

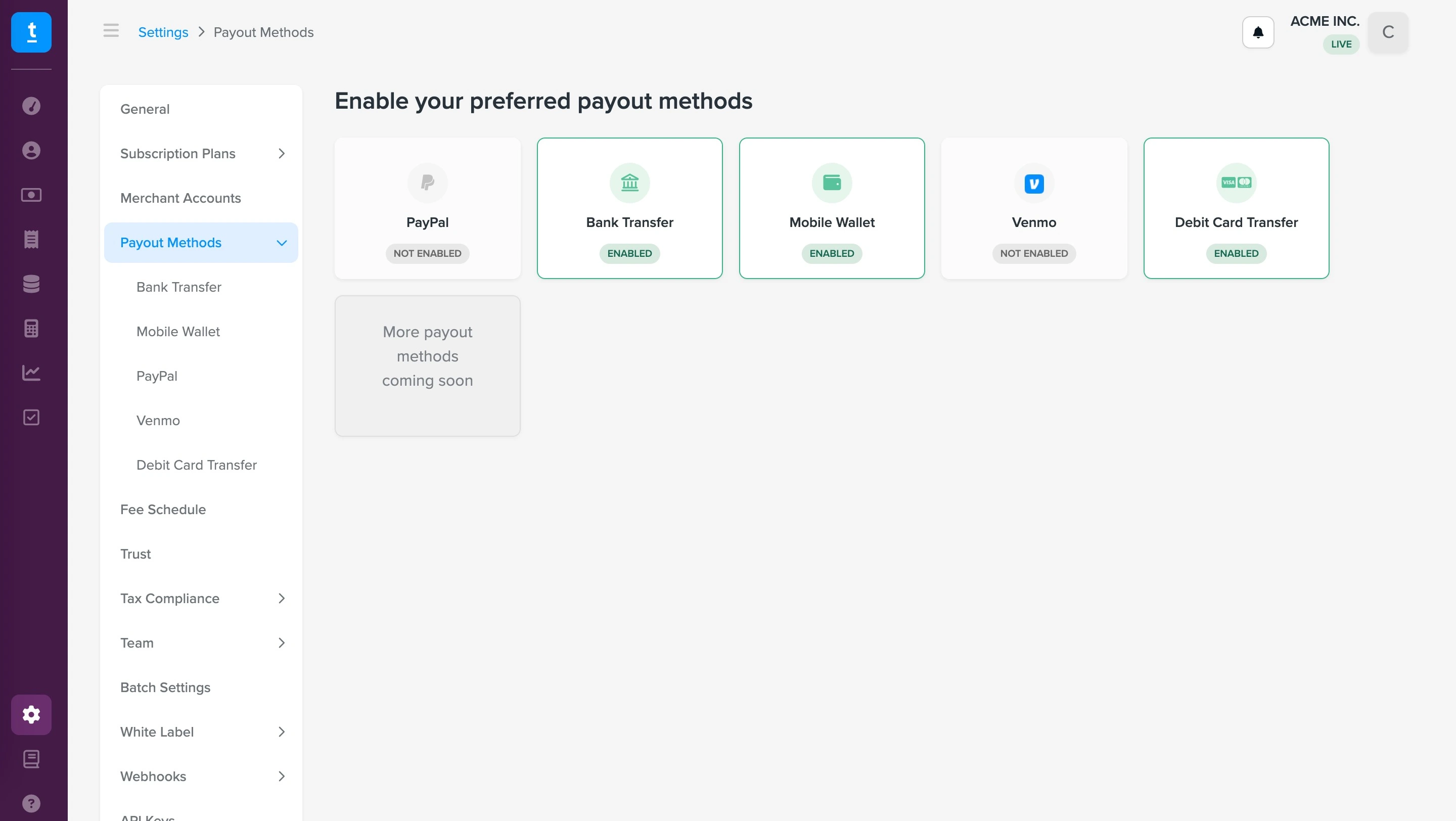

To get started using debit card payouts, go to your dashboard and navigate to Settings→ Payout Methods, where you can enable Debit Card Payouts for your account. This option is currently available to US merchants on Cross River Bank.

Once enabled, you can configure how the method is offered to recipients and review your fee settings. Debit card payouts use a percentage-based fee model (1.00% per payout with a $1.50 minimum), and you can choose how much of that fee to cover on behalf of recipients—either as a fixed amount or a percentage, with optional caps to control costs on your end.

From there, recipients will be able to add and verify their debit card directly in the portal and select it as their payout method. Clear status visibility and near-instant processing help set expectations and reduce follow-up questions.

For more detailed guidance, you can refer to our help documentation to review the full breakdown of fees and reconciliation, or explore the developer documentation for API integration and webhook handling.

Raise the bar on payouts and recipient experience

Payouts aren’t just operational—they shape how recipients experience your product.

By adding debit card payouts, you’re giving recipients more control over how they get paid, reducing friction, and improving trust across the payout lifecycle.

Explore other new releases to see how we’re continuing to improve payouts across speed, flexibility, and control.

Global standards. Local choice.